Cost of production

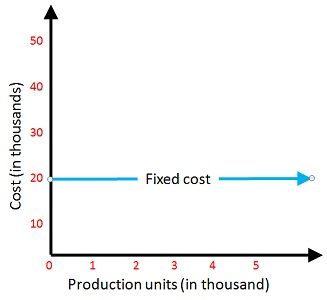

- Fixed cost: A costs that does not change no matter how much is produced

Ex: Mortgage

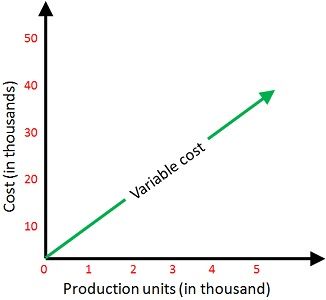

Ex: Mortgage- Variable Costs- A cost that rises or falls depending on how much is produced

Ex: Electricity bills

Ex: Electricity bills

- Total Costs: Fixed Costs + Variable Costs

- Marginal Revenue: Additional income from selling one more unit of a good.

- Marginal Costs: The cost of producing one more unit of a good.

- Total Revenue: Price x Quantity

Go to:

No comments:

Post a Comment